Learn how to enhance your trading strategies by maximizing your Sharpe Ratio through effective risk management and return optimization techniques.

The Sharpe Ratio measures how well your trading strategy balances returns and risk. A higher Sharpe Ratio means better risk-adjusted performance. Here's how to improve it:

-

Increase Returns (Rp):

- Time trades effectively using indicators like MACD, RSI, and Bollinger Bands.

- Diversify your portfolio with low-correlation assets and alternative investments.

- Reduce trading costs by using limit orders, trading during high-liquidity periods, and choosing low-fee brokers.

-

Control Risk (σp):

- Manage position sizes based on volatility.

- Use stop-loss orders set 2-3 times the Average True Range (ATR).

- Apply risk parity to evenly distribute risk across positions.

-

Use Tools:

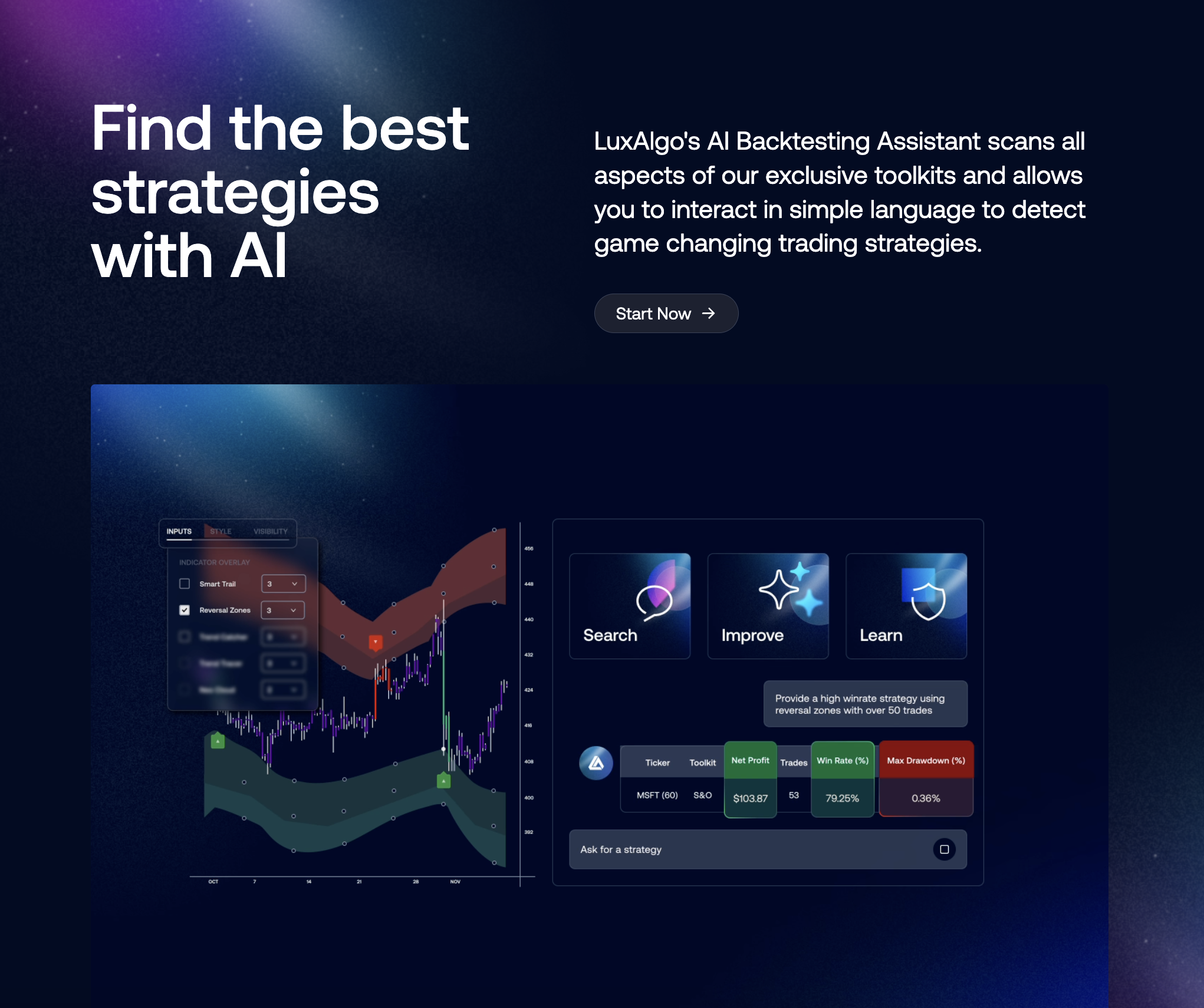

- Backtest strategies with LuxAlgo’s AI Backtesting Assistant.

- Monitor trades with automated alerts and historical data testing.

-

Regular Reviews:

- Measure your Sharpe Ratio annually and adjust based on results.

- Test strategies across different timeframes and market conditions.

Start by calculating your current Sharpe Ratio and apply these steps to improve both returns and risk management. A Sharpe Ratio above 1.0 is good; aim for higher to optimize your trading strategy.

The Sharpe Ratio Explained

Increasing Returns for Better Sharpe Ratio

Boosting returns involves three formula-driven strategies aimed at increasing Rp in the Sharpe Ratio formula: S = (Rp - Rf)/σp. These methods focus on improving the numerator (Rp) while carefully managing the denominator (σp). We'll dive deeper into managing risk in the "Risk Control Methods" section.

Trade Entry and Exit Timing

Timing trades effectively requires blending technical signals with liquidity patterns. Analyzing multiple timeframes helps align short-term trades with larger market trends. Focus on setups where multiple indicators confirm the trade direction for higher success rates.

Here's a quick reference for key technical indicators and their optimal use:

| Indicator | Primary Use | Confirmation Signals |

|---|---|---|

| MACD | Trend Direction | Crossover above/below signal line |

| RSI | Overbought/Oversold | Values above 70 or below 30 |

| Bollinger Bands | Volatility Range | Price touching upper/lower bands |

| Volume Analysis | Trade Confirmation | Volume surge with price movement |

Use at least two independent indicators to validate trade entries. For instance, combining an RSI showing oversold conditions with a positive MACD divergence strengthens the entry signal more than relying on a single indicator alone[1].

Portfolio Asset Mix

Choose assets with low correlation (below 0.5) and positive expected returns across various sectors and regions. To achieve better diversification:

- Spread investments across multiple sectors and geographic areas.

- Include alternative assets like REITs or managed futures[3].

- Rebalance regularly to maintain your target allocation.

This approach not only reduces portfolio volatility (σp) but also supports return growth (Rp), improving the Sharpe Ratio on both fronts.

Reducing Trading Costs

Cutting trading costs can significantly impact your portfolio's overall performance. Key cost-saving measures include:

- Using limit orders and trading during high-liquidity periods to lower spreads by up to 20%.

- Choosing brokers offering lower fees (0.1-1% per trade) and maker rebates.

For example, a strategy with 10% returns and 15% volatility could see its Sharpe Ratio rise from 0.67 to 0.77 by reducing trading costs by just 1.5% annually[1][4]. Volume-based fee structures can further slash execution costs[4]. When combined with proper position sizing (discussed next), these savings can compound to enhance your Sharpe Ratio even more.

Risk Control Methods

Managing risk effectively can help lower portfolio volatility (σp) while maintaining returns, which improves the Sharpe Ratio. Since the Sharpe Ratio is calculated as (Rp - Rf)/σp, reducing σp strengthens the denominator without compromising returns.

Position Size Management

Position sizing plays a critical role in managing risk-adjusted returns. Research has shown that proper position sizing can cut average drawdowns by 37% over a 12-month period across 1,000 trading accounts [2].

Here’s how to approach it:

- Adjust position sizes based on asset volatility.

- Limit exposure to correlated assets to avoid compounding risk.

- Gradually scale into positions to manage risk more effectively.

For assets with higher volatility, reducing position sizes can help maintain consistent risk levels. Use historical price data to guide these adjustments.

Stop-Loss Strategy

Strategic stop-loss orders are essential for limiting losses while still allowing room for potential gains. Volatility-based stops are particularly effective, often set at 2-3 times the Average True Range (ATR) below the entry price for long trades [1].

The LuxAlgo platform’s support and resistance indicators can help place stops at meaningful technical levels, avoiding random placements. Combining these stop-loss strategies with well-timed entries and exits strengthens overall risk management.

Risk-Return Balance

Striking the right balance between risk and return is critical for optimizing the Sharpe Ratio. Overly aggressive risk reduction can hurt returns, while excessive risk-taking increases σp. A practical solution is risk parity, where each position contributes equally to the portfolio’s overall risk, rather than allocating equal dollar amounts [1].

To refine your risk control, consider these techniques:

- Adjust position sizes inversely to volatility spikes to stabilize risk exposure.

- Rebalance your portfolio with correlation in mind to reduce overlapping risks.

- Use risk parity allocation to distribute risk evenly across positions.

Tools for Sharpe Ratio Analysis

Sharpe Ratio optimization becomes more efficient with the right tools. These tools simplify the process, making it easier to balance returns and risk effectively.

LuxAlgo Platform Features

The LuxAlgo platform offers a range of features designed to enhance both components of the Sharpe Ratio. The Price Action Concepts (PAC) feature refines entry and exit points using pattern recognition, while its volatility metrics help with accurate position sizing. These features target both the returns (numerator) and the risk (denominator) in the Sharpe Ratio formula.

Another key feature is the Oscillator Matrix (OSC), which combines multiple indicators and uses automated divergence detection to confirm trading signals.

For traders building advanced strategies, LuxAlgo's AI Backtesting Assistant allows testing strategies under various market conditions, providing valuable insights for optimization [2].

Testing with Historical Data

Even with real-time features from LuxAlgo, validating strategies with historical data is essential. This process ensures strategies are robust across different scenarios:

- Data Segmentation: Analyze performance across diverse market conditions to identify strengths and weaknesses.

- Monte Carlo Simulation: Test strategies through multiple simulated scenarios to uncover potential risks that could affect the Sharpe Ratio.

- Factor in trading costs, such as commissions and slippage, for a realistic assessment.

Alert System Setup

LuxAlgo's integration with TradingView makes it possible to set up automated alerts for trading signals. These alerts can be customized based on specific conditions, ensuring consistent execution of strategies.

Examples of alerts include:

- Triggers based on price movements that align with your strategy.

- Volatility thresholds to manage risk effectively.

This structured approach helps traders make steady improvements to their Sharpe Ratio.

Step-by-Step Optimization Guide

Current Sharpe Ratio Measurement

To begin, determine your strategy's baseline Sharpe Ratio. You'll need at least a year of trading data for accuracy. Using daily returns data, follow these steps:

- Find the average daily return of your strategy.

- Subtract the risk-free rate from the average return.

- Divide by the standard deviation of the returns.

- Multiply by the square root of 252 trading days to annualize the result.

For instance, if your strategy delivers a 12% annual return, a 3% risk-free rate, and a 15% standard deviation, the Sharpe Ratio would be 0.6. This serves as your benchmark for any improvements.

Timeframe Analysis

Timeframe analysis plays a crucial role in refining your Sharpe Ratio. By using longer timeframes, you can reduce market noise, which directly improves the denominator (σp) in the Sharpe Ratio calculation.

Here’s how you can approach different timeframes:

Short-term (Intraday)

- Test intervals such as 5 minutes to 1 hour while factoring in transaction costs.

- Analyze how costs affect net returns.

- Use multiple oscillators to evaluate signal quality.

Medium-term (Swing)

- Study daily and weekly patterns.

- Identify periods of clustered volatility.

- Compare risk-adjusted returns across various holding periods.

Weekly timeframes often outperform daily trading in terms of Sharpe Ratio. They help reduce noise and lower transaction costs, making them a preferred choice for many strategies.

Strategy Testing Methods

To ensure your strategy holds up under different market conditions, use rolling window analysis. This approach helps you evaluate consistency in your Sharpe Ratio over time.

Key Testing Parameters:

- Use 12-month rolling windows with monthly shifts.

- Apply monthly step sizes to capture seasonal trends.

- Set a minimum performance threshold - your Sharpe Ratio should exceed 1.0 in at least 80% of the windows.

Leverage backtesting features to automate testing across various assets and timeframes. For example, combining volatility metrics with 20-day moving averages has shown to improve the median Sharpe Ratio by 22% in backtests, thanks to a better signal-to-noise ratio.

Summary and Next Steps

Once you've applied these optimization steps, the key to sustained success lies in consistent execution and frequent performance evaluations.

Risk and Return Management

Optimizing the Sharpe Ratio means finding the right balance between risk and returns. To achieve this, focus on building a diversified portfolio with assets that don't move in sync. At the same time, enforce strict position sizing rules to ensure better risk-adjusted outcomes [1].

Tool Implementation

To keep these improvements on track, consider integrating the following features into your workflow:

- Screeners: Spot high-probability trading opportunities.

- Backtesting Tools: Test your strategy to ensure it holds up under different scenarios.

- Alert Systems: Stay disciplined by receiving timely notifications.

The LuxAlgo platform offers a powerful set of features to support this process. For example, the Price Action Concepts (PAC) feature helps fine-tune entry and exit points, while the Oscillator Matrix detects real-time divergences, improving your decision-making timing [5].

Ongoing Strategy Review

To keep your strategy effective, schedule regular performance reviews. Using LuxAlgo's AI Backtesting Assistant, you can analyze your approach across varying market conditions. Focus on these key areas:

- Conduct quarterly backtests to account for changing market trends.

- Reassess position sizing based on updated volatility data.

- Monitor how trading costs impact your overall returns.