Understanding survivorship bias in backtesting is crucial for realistic trading strategy evaluation and risk assessment.

Survivorship bias in backtesting can distort trading strategies by ignoring failed or delisted assets, leading to inflated returns and underestimated risks. For example, excluding defunct stocks from historical data can overstate annual returns by 1-4% and skew performance metrics like Sharpe ratios and drawdowns.

Key Takeaways:

- What is Survivorship Bias? Only analyzing surviving assets, ignoring those that failed or were delisted.

- Impact on Results: Overstated returns (~0.9% annually for mutual funds), underestimated risks (14% drawdown underestimation), and skewed performance metrics.

- Examples: Momentum strategies and sector-focused models often show inflated results due to this bias.

- Solutions: Use point-in-time data, include delisted assets, and leverage advanced backtesting platforms for accurate analysis.

By addressing survivorship bias with proper data and advanced features, traders can create more realistic and reliable strategies.

Survivorship Bias In Trading (How To Avoid It)

Effects on Backtest Results

Data Sources and Bias

Survivorship bias can heavily distort trading data, especially when historical records are affected by significant market events. For example, companies involved in mergers, acquisitions, or bankruptcies often disappear from databases, leaving an incomplete picture of past market conditions. A notable instance is the dot-com bubble burst in the early 2000s, where many tech companies failed or were delisted, creating gaps in the data [5].

This bias primarily arises from two factors:

- Index Reconstitutions: Data from the CRSP US Stock Database highlights this issue. It shows annualized returns of 7.4% in survivorship-free datasets versus 9.0% in survivorship-biased ones (1926–2001), a 1.6% difference [3].

- Delisted Securities: Over time, the exclusion of delisted securities compounds distortions, further skewing analyses.

Distorted Performance Metrics

Survivorship bias can significantly alter performance metrics that traders depend on to evaluate strategies. The effects are particularly noticeable in areas like risk assessment and performance evaluation.

- Risk-Adjusted Returns: Research by Brown, Goetzmann, Ibbotson, and Ross found that survivorship bias could inflate Sharpe ratios by as much as 0.5 points [3]. Considering that a Sharpe ratio of 1.0 is viewed as strong performance, this inflation is substantial.

- Maximum Drawdowns: A study by Andrikogiannopoulou and Papakonstantinou showed that survivorship bias caused an average underestimation of hedge fund drawdowns by 14 percentage points [6]. This makes strategies appear less risky than they actually are.

| Metric | Bias Impact |

|---|---|

| Sharpe Ratio | Up to 0.5 points inflation |

| Maximum Drawdown | 14 percentage points underestimation |

These distortions are especially pronounced during market crises. For instance, Bianchi and Koutmos discovered that survivorship bias led to a 2.1% annual overestimation of mutual fund performance during the 2008 financial crisis [7]. Such inaccuracies can undermine the reliability of backtesting results, emphasizing the importance of including comprehensive data for effective strategy evaluation.

Identifying Survivorship Bias

Spotting Issues in Performance Data

Uncovering survivorship bias in backtest results requires a close look at performance details. One big red flag? Unrealistically high returns that outshine established market benchmarks. For instance, a survivorship-biased analysis of mutual funds might show annual returns inflated by 2.1% simply by excluding failed funds [1].

Another clue is overly smooth equity curves with barely any drawdowns. When failed trades are left out, the performance looks far more stable than it really is.

| Warning Sign | Common Bias Effect |

|---|---|

| Inflated Returns | Up to 2.1% higher annual returns |

| Downplayed Risk | Up to 14% fewer drawdowns |

Real-World Strategy Failures

Examples of strategies derailed by survivorship bias offer critical insights. One case involves momentum strategies that rely on past performance but ignore delisted stocks. This issue is similar to the S&P 500 reconstitution problem, showing how survivorship bias can creep into various strategy types.

A 2021 hedge fund strategy published on Seeking Alpha fell into this trap. It chose stocks based on the past success of top-performing funds but only considered funds that survived from 2008 to 2021, introducing significant bias [1].

Sector-specific strategies are especially vulnerable. For example, technology-focused strategies that overlook failures from the dot-com bubble often show inflated returns, particularly in backtests.

"Most listed companies fail to beat short-term Treasury bills", says Hendrik Bessembinder's research [1], emphasizing how survivorship bias can hide the real challenges of achieving consistent returns.

Common pitfalls include:

- Value investing strategies that ignore bankrupt companies

- High-frequency trading models relying on incomplete historical data [2]

Advanced backtesting tools help traders gain a realistic view of strategy performance across varying market conditions.

Tools and Software Solutions

Modern backtesting platforms tackle survivorship bias by offering:

- Comprehensive databases covering both active and delisted assets

- Automated systems to detect potential biases

- Simulations based on point-in-time data

- Tools for customizing universe selection

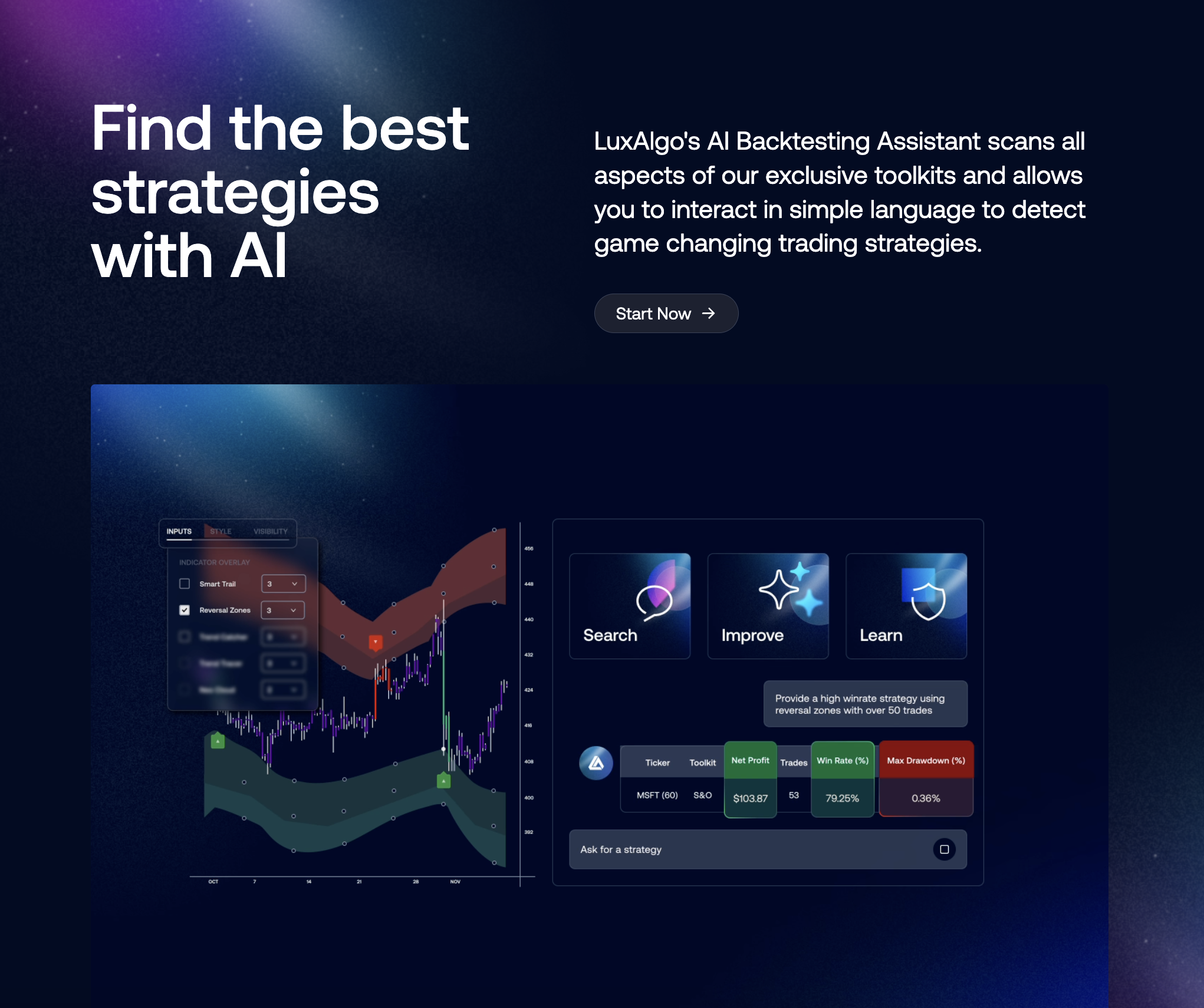

LuxAlgo AI Backtesting Assistant

LuxAlgo's AI Backtesting Assistant is a dynamic feature of the provider’s exclusive offerings, designed to help traders overcome challenges like survivorship bias. By leveraging comprehensive databases that include both active and delisted assets, the AI Backtesting Assistant identifies potential biases, simulates realistic market conditions, and delivers detailed performance metrics.

This advanced feature integrates seamlessly into your strategy development process—whether you are a beginner or an experienced trader—providing insights that help fine-tune trading strategies with accurate, real-world data.

Conclusion

Accurate Testing Methods

To address survivorship bias effectively, traders need to rely on solid data sources and precise detection features. This type of bias can skew performance estimates by as much as 4-6% annually [1]. A striking example occurred in 2010 when Quantitative Investment Management (QIM) discovered that their strategy's actual returns were only 8%, far below the projected 20%, once survivorship bias was properly accounted for.

As highlighted throughout this guide, using databases that include both active and defunct securities is crucial for achieving dependable results.

Strategy Testing Best Practices

For reliable strategy development, it's critical to follow these key practices:

- Data Quality: Use point-in-time databases that include both active and delisted assets. This can reduce overestimation by around 2% annually [1].

- Validation: Incorporate out-of-sample testing and forward validation to ensure accuracy.

- Risk Assessment: Apply Monte Carlo simulations and stress testing to evaluate potential risks.

By combining these methods with considerations like transaction costs, traders can build strategies that are more reliable and aligned with market realities.

"The combination of comprehensive data sources and advanced testing methodologies is essential for developing trading strategies that perform consistently in live market conditions", says Marcos Lopez de Prado in Advances in Financial Machine Learning (2018).

FAQs

What are the biases in backtesting?

Backtesting can be affected by several biases, including survivorship bias (ignoring failed assets), look-ahead bias (using future data inappropriately), and overfitting (over-optimizing for historical data). Survivorship bias is especially problematic, as it can inflate annual returns by 1-4% and has a compounding effect over time, leading to skewed results.

Is backtesting a survivor bias?

No, backtesting itself isn't inherently biased. However, it is prone to survivorship bias if not handled carefully. Ignoring delisted or failed companies in the dataset can lead to unrealistic strategy evaluations and misleading performance metrics.

How do you get rid of survivorship bias?

To minimize survivorship bias, traders can take these steps:

- Use databases that are free from survivorship bias

- Keep accurate historical records of asset constituents

- Incorporate Monte Carlo simulations for broader testing scenarios

Leveraging advanced backtesting platforms can help ensure better data quality and more realistic strategy evaluations.